Earning a salary of ₹20,000 might look limited when you think about all the expenses, but with a little planning, discipline, and the right mindset, it is absolutely possible to manage your daily needs while also saving and investing for the future. The trick is not about how much you earn, but how well you use what you earn.

- Start with the 50-30-20 Rule

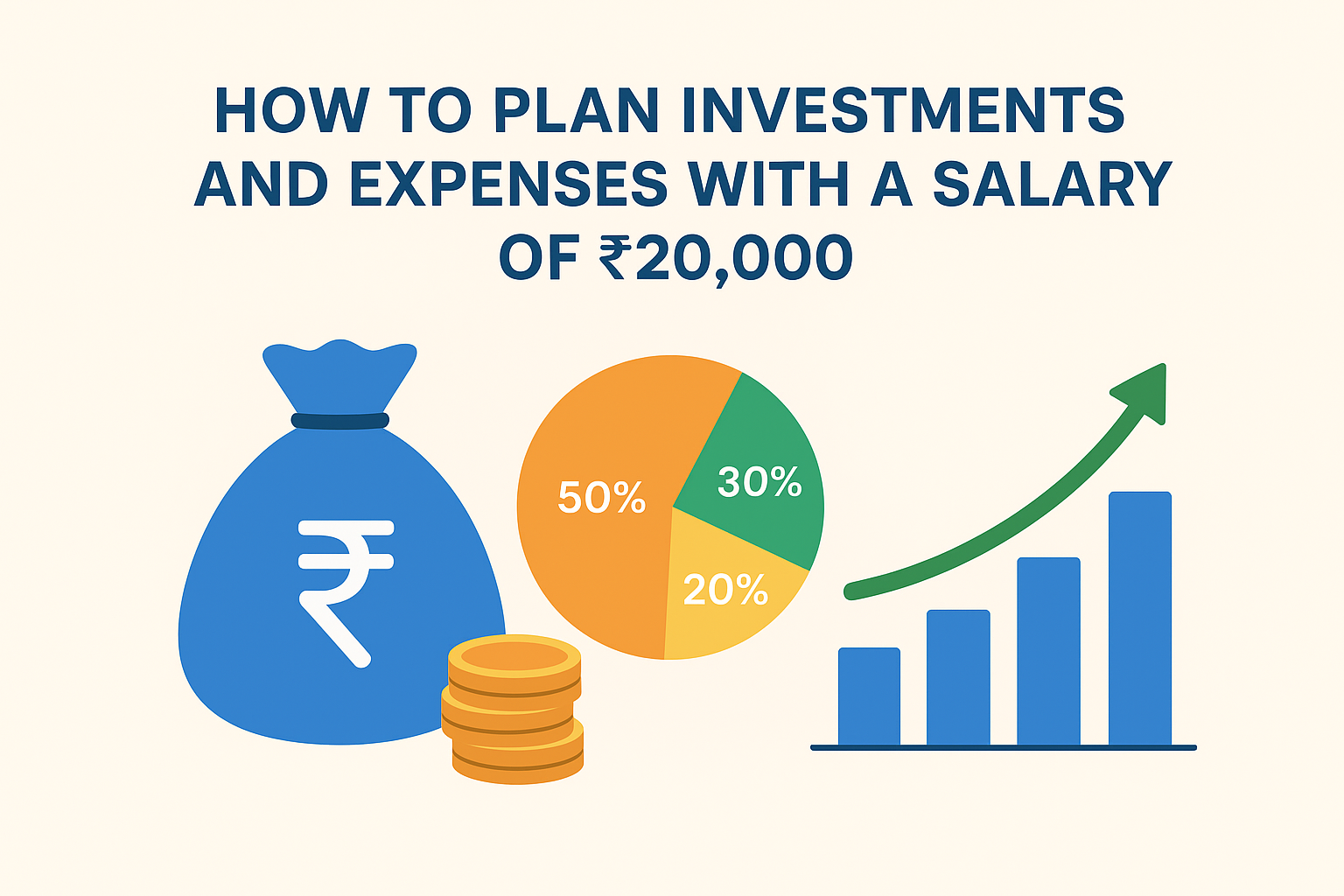

A simple way to balance spending and saving is by following the 50-30-20 budgeting rule:

50% Needs (₹10,000): Rent, groceries, transport, electricity, and basic essentials.

30% Wants (₹6,000): Shopping, entertainment, outings, and hobbies.

20% Savings & Investments (₹4,000): SIPs, insurance, emergency fund, or other investments.

This method ensures that your essentials are taken care of, you enjoy your lifestyle, and still put aside money for the future.

- Build an Emergency Cushion

Unexpected events like job loss, medical expenses, or family emergencies can disrupt your finances. That’s why you should aim to create an emergency fund equal to 3–6 months of your income. Start small, even ₹500–₹1,000 per month, and keep it in a separate savings account or liquid investment so you don’t touch it unnecessarily.

- Keep Daily Expenses Under Control

Managing expenses wisely makes a huge difference. A few smart choices can save you thousands every month:

Cook at home more often instead of eating out.

Use public transport or shared rides to cut travel costs.

Limit impulse shopping, especially online.

Choose budget-friendly mobile/data plans.

These small adjustments can easily save ₹2,000–₹3,000 every month.

- Begin Small but Consistent Investments

Even if your income is modest, consistency matters more than the amount. Options you can consider:

Mutual Fund SIPs (₹500–₹2,000/month): Long-term wealth building with compounding.

Recurring Deposit: Safe and disciplined savings with fixed returns.

PPF (Public Provident Fund): Great for long-term tax-saving and guaranteed growth.

Gold (digital or SIP): A hedge against inflation and a stable investment.

Starting small today creates big results tomorrow.

- Secure Yourself with Insurance

Insurance is not an expense; it’s protection.

Health Insurance: Covers unexpected medical bills, preventing financial stress.

Term Insurance: If you have dependents, this ensures their financial safety.

Even affordable basic plans can provide peace of mind.

- Clear Debts Quickly

If you have loans or credit card dues, clear them as early as possible. High-interest debt eats into your salary and delays financial progress. Avoid unnecessary borrowing and learn to live within your means.

- Find Ways to Increase Your Income

Saving alone is not enough—growing your income helps you save and invest more. You can try:

Freelancing skills like writing, designing, or teaching online.

Part-time weekend jobs.

Learning new skills through online courses to boost career opportunities.

Every extra rupee earned can be turned into future wealth.

- Track and Review Every Month

The final step is to review your money flow every month. Check:

How much you spent on needs and wants.

How much you saved and invested.

Areas where you can cut down next month.

Use a simple notebook, Excel sheet, or finance app to stay disciplined.

Final Thoughts

A salary of ₹20,000 may feel restrictive, but with proper money management, you can balance expenses, build savings, and start investing for your future. The key lies in discipline, consistency, and planning ahead. Remember, financial success doesn’t depend on how much you earn—it depends on how smartly you handle it.

Start today, and your future self will thank you. 🌱