A strong credit score is the key to financial stability. In India, the CIBIL score ranges between 300 and 900, and it acts as a benchmark for banks and lenders when approving loans or credit cards. A score of 750 and above is generally considered excellent and improves your chances of getting loans at lower interest rates.

If you are struggling with a low score or want to enhance it further, here are some practical tips to improve your CIBIL score.

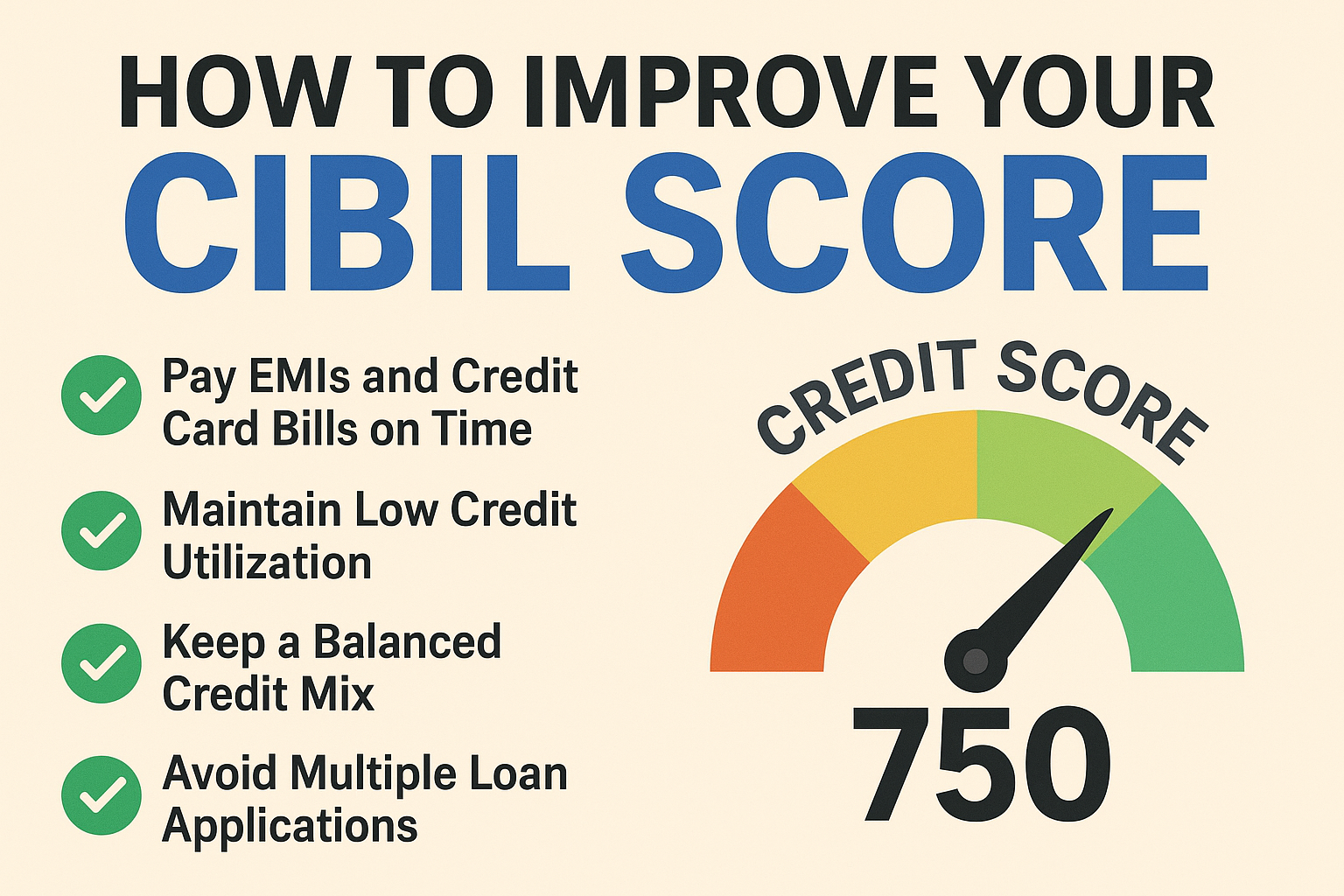

✅ 9 Effective Tips to Improve Your CIBIL Score

- Pay EMIs and Credit Card Bills on Time

Timely repayment is the most crucial factor in boosting your score. Even one late payment can impact your profile negatively.

💡 Tip: Set reminders or auto-debit instructions to avoid missing due dates.

- Maintain Low Credit Utilization

Using too much of your available credit limit signals financial dependency. Try to keep your credit usage below 30–40% of the total limit.

💡 Tip: Distribute expenses across multiple cards.

- Keep a Balanced Credit Mix

Lenders prefer a healthy balance of secured loans (like home or car loans) and unsecured loans (like personal loans and credit cards). Too many unsecured loans can reduce your score.

- Avoid Multiple Loan Applications

Every new loan or card application generates a hard inquiry. Frequent inquiries make you look credit-hungry, which lowers your score.

💡 Tip: Apply only for the credit you genuinely need.

- Monitor Your Credit Report

Errors in your credit report, such as incorrect loan entries or uncleared balances, may reduce your score.

💡 Tip: Check your CIBIL report regularly and raise disputes for incorrect details.

- Keep Old Accounts Active

The longer your credit history, the better. Closing old accounts may shorten your credit history and lower your score.

💡 Tip: Keep your oldest card or account active with minimal usage.

- Increase Your Credit Limit (Use Wisely)

A higher limit with controlled spending reduces your credit utilization ratio, which helps your score grow.

- Clear Outstanding Dues and Settlements

Any pending dues or loan settlements harm your creditworthiness. Clearing them boosts your CIBIL score gradually.

- Stay Consistent and Patient

CIBIL score improvement is a long-term process. Consistency in good financial habits will show results within 6–12 months.

📌 20 FAQs on Improving CIBIL Score

- What is a good CIBIL score?

A score of 750 or above is considered good for getting loans easily. - How long does it take to improve a CIBIL score?

With consistent repayment and low utilization, it usually takes 6 to 12 months. - Does checking my own CIBIL score reduce it?

No. Self-checks are called soft inquiries and do not affect your score. - Can paying only the minimum credit card amount improve my score?

No. Always pay the full bill amount; paying only the minimum increases debt. - Do loan settlements harm the CIBIL score?

Yes, settled loans are seen as unpaid and reduce your score. - Can applying for multiple credit cards lower my score?

Yes, multiple applications generate hard inquiries and impact your score. - Does closing a credit card help improve CIBIL score?

Not always. Closing old cards may reduce your credit history length. - How often should I check my CIBIL report?

At least once a year to detect and correct errors. - Does increasing a credit limit improve the score?

Yes, if you use it wisely and keep utilization low. - Can overdue payments be removed from my CIBIL report?

No, they remain for up to 7 years, but regular timely payments will reduce their effect over time. - Will taking a personal loan improve my score?

Yes, if repaid on time, it shows credit discipline. - Can a low CIBIL score be improved quickly?

There are no shortcuts. Improvement requires consistent financial discipline. - Is a secured loan better for improving credit score?

Yes, secured loans like home or car loans with timely repayment boost credit history. - What is the fastest way to improve CIBIL score?

Paying all dues on time and maintaining low credit utilization. - Does defaulting on EMI permanently damage my score?

No, but defaults stay in your report for years and lower your score significantly. - Do joint loans affect my score?

Yes, any missed EMI in a joint loan impacts all co-borrowers’ CIBIL scores. - Can I improve my score if I have no credit history?

Yes, by responsibly using a credit card or taking a small loan. - What happens if I never use my credit card?

Inactivity doesn’t directly lower your score, but active usage with timely repayment is better. - Can too many unsecured loans reduce my score?

Yes, they show financial dependency and may hurt your score. - What is the ideal credit utilization ratio?

Keep it below 30% of your total credit limit.

📢 Final Thoughts

Improving your CIBIL score is not difficult if you stay disciplined. Pay bills on time, keep credit usage low, maintain a healthy credit mix, and avoid unnecessary applications. With consistent effort, you can boost your score and enjoy better financial opportunities.