The Indian government has launched several initiatives to make financial protection accessible to everyone, especially those with limited income. Two of the most beneficial insurance schemes available today are the Pradhan Mantri Suraksha Bima Yojana (PMSBY) and the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY).

These plans offer basic insurance coverage at very low annual costs. However, many individuals are unsure about the difference between the two or which one they should choose. In this article, we’ll simplify both plans by explaining their coverage, cost, eligibility, and benefits—so you can decide what suits your needs best.

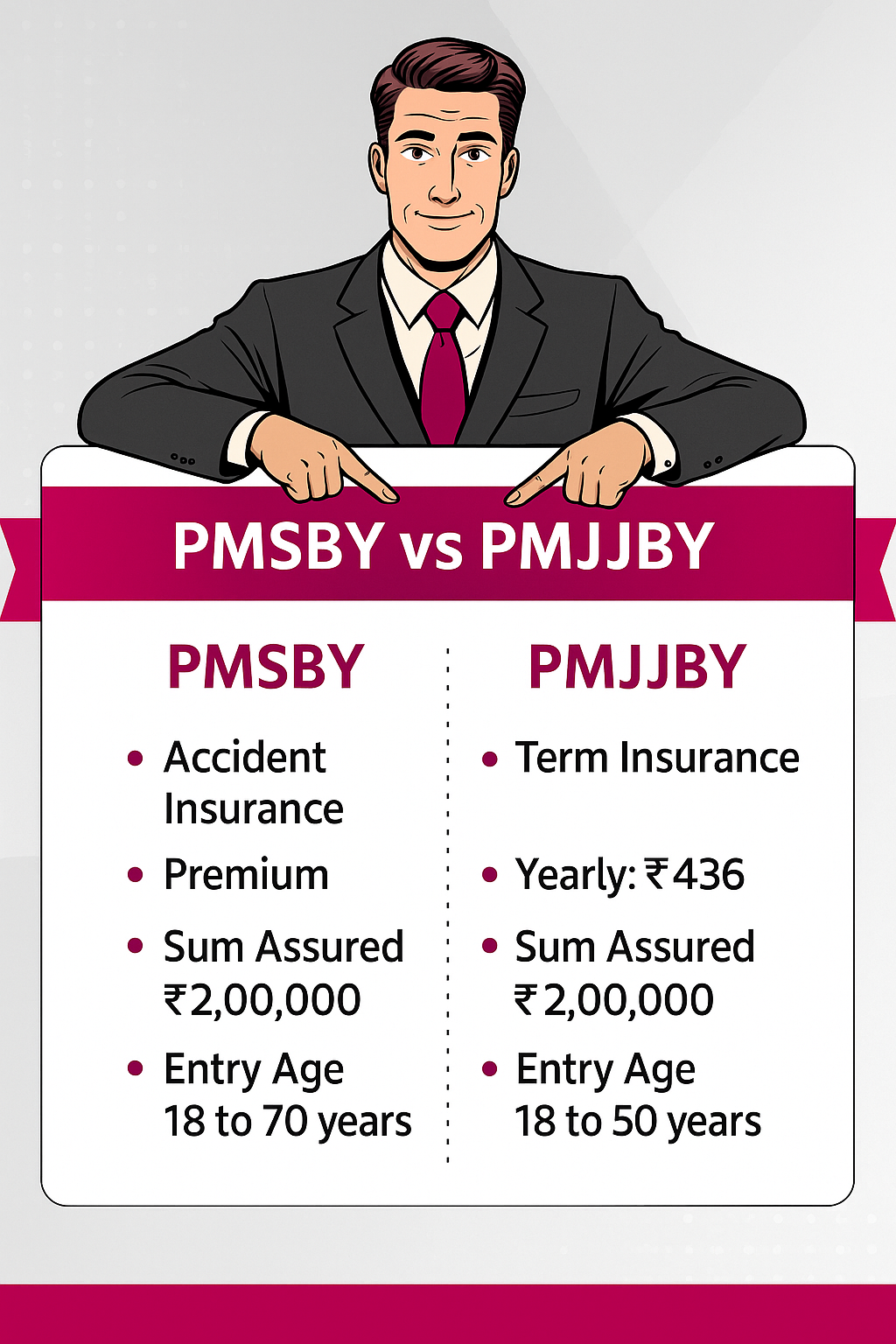

🌟 What Is PMSBY?

Pradhan Mantri Suraksha Bima Yojana (PMSBY) is a personal accident insurance scheme that provides financial support in the case of death or disability caused by an accident. This scheme is ideal for individuals who want accident protection but cannot afford traditional insurance policies.

Key Highlights of PMSBY:

- Insurance Type: Accidental death and disability cover

- Yearly Premium: ₹20

- Coverage Amount: ₹2,00,000

- Eligible Age Group: 18 to 70 years

- Exit Age: Coverage renewable till age 70

- Policy Period: Valid from June 1 to May 31 (renewable annually)

- Availability: Open to all savings account holders

- Insurance Provider: TATA AIG General Insurance Co. Ltd.

- How to Join: Via bank branch using EASYPAY system

Benefits:

- In case of accidental death, nominee gets ₹2 lakh

- Full disability (e.g., loss of both hands/eyes): ₹2 lakh

- Partial disability (e.g., loss of one hand/eye): ₹1 lakh

- Affordable for daily wage earners and low-income families

🌟 What Is PMJJBY?

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is a pure term life insurance plan. This scheme offers financial support to the policyholder’s family in the unfortunate event of their death—whether due to illness, accident, or natural causes.

Key Highlights of PMJJBY:

- Insurance Type: Life insurance plan (covers all causes of death)

- Yearly Premium: Varies by quarter

- ₹436 (June–Aug)

- ₹342 (Sept–Nov)

- ₹228 (Dec–Feb)

- ₹114 (Mar–May)

- Coverage Amount: ₹2,00,000

- Eligible Age Group: 18 to 50 years

- Exit Age: Renewable until 55 years

- Policy Period: June 1 to May 31 (renewable yearly)

- Availability: All savings account holders are eligible

- Insurance Providers: Max Life Insurance Co. Ltd. & Bajaj Allianz Life

- How to Join: Through your bank branch using EASYPAY

Benefits:

- Covers death due to any cause (accident, illness, or natural)

- ₹2 lakh is paid to the nominee

- Peace of mind for families of salaried and self-employed individuals

- Minimal premium, high coverage

🔍 PMSBY vs PMJJBY – A Detailed Comparison

| Feature | PMSBY | PMJJBY |

|---|---|---|

| Type of Insurance | Accident cover | Term life insurance |

| Coverage Type | Accidental death/disability | Death due to any cause |

| Sum Insured | ₹2,00,000 | ₹2,00,000 |

| Entry Age | 18 to 70 years | 18 to 50 years |

| Exit Age | Up to 70 years | Up to 55 years |

| Annual Premium | ₹20 | ₹114–₹436 (depends on quarter) |

| Availability | Savings account holders | Savings account holders |

| Insurer | TATA AIG General Insurance | Max Life & Bajaj Allianz Life |

| Enrolment Method | Through bank (EASYPAY mode) | Through bank (EASYPAY mode) |

💡 Who Should Choose These Plans?

- If you’re between 18 and 50 years old, it’s a good idea to enroll in both PMSBY and PMJJBY for full protection.

- PMSBY is perfect for workers or laborers who are often exposed to physical risk.

- PMJJBY is ideal for those who want their family financially protected in case of their untimely death.

- Since the premiums are extremely low, both schemes are highly suitable even for people with limited income.

📝 How to Enroll?

Here’s a simple step-by-step process:

- Visit your bank where your savings account is maintained.

- Ask for the PMSBY/PMJJBY enrollment form.

- Fill in your personal and nominee details.

- Submit the form at the branch.

- The annual premium will be automatically debited from your account.

Your insurance becomes active from June 1st and remains valid until May 31st the following year.

⚠️ Key Points to Keep in Mind

- PMSBY only covers accidental cases. Natural death is not included.

- PMJJBY covers all types of death but has an age limit of 55 for renewal.

- Your insurance will end if your savings account is closed or if you cross the exit age.

- Ensure your Aadhaar is linked to your bank account for a hassle-free experience.

❓FAQs – Frequently Asked Questions on PMSBY & PMJJBY

Q1: Can I subscribe to both PMSBY and PMJJBY at the same time?

Yes, you can take both policies if you fall within the eligible age brackets. This way, you get coverage for both accidental and natural death.

Q2: Will the policy be renewed automatically every year?

Yes, if your bank account has sufficient balance, the premium will be auto-debited annually, and your policy will continue without interruption.

Q3: Can I enroll in these schemes online?

Currently, enrollment is done through your bank branch via the EASYPAY system. Some banks may offer online forms depending on their setup.

Q4: What if I don’t have a nominee?

Having a nominee is highly recommended. If no nominee is registered, the claim process can be delayed in case of a payout.

Q5: Is there any tax benefit for these schemes?

No, PMSBY and PMJJBY do not directly offer tax benefits under Section 80C or 10(10D) of the Income Tax Act. However, the payout received by the nominee is tax-free.

🔚 Final Thoughts

For just a few hundred rupees a year, PMSBY and PMJJBY together offer financial coverage worth ₹4 lakhs. These government-backed schemes are designed to protect common citizens and their families from financial hardships in case of sudden loss or accidents.

If you’re eligible, don’t delay—visit your bank and enroll today. A small step now can ensure your loved ones are supported when they need it the most.