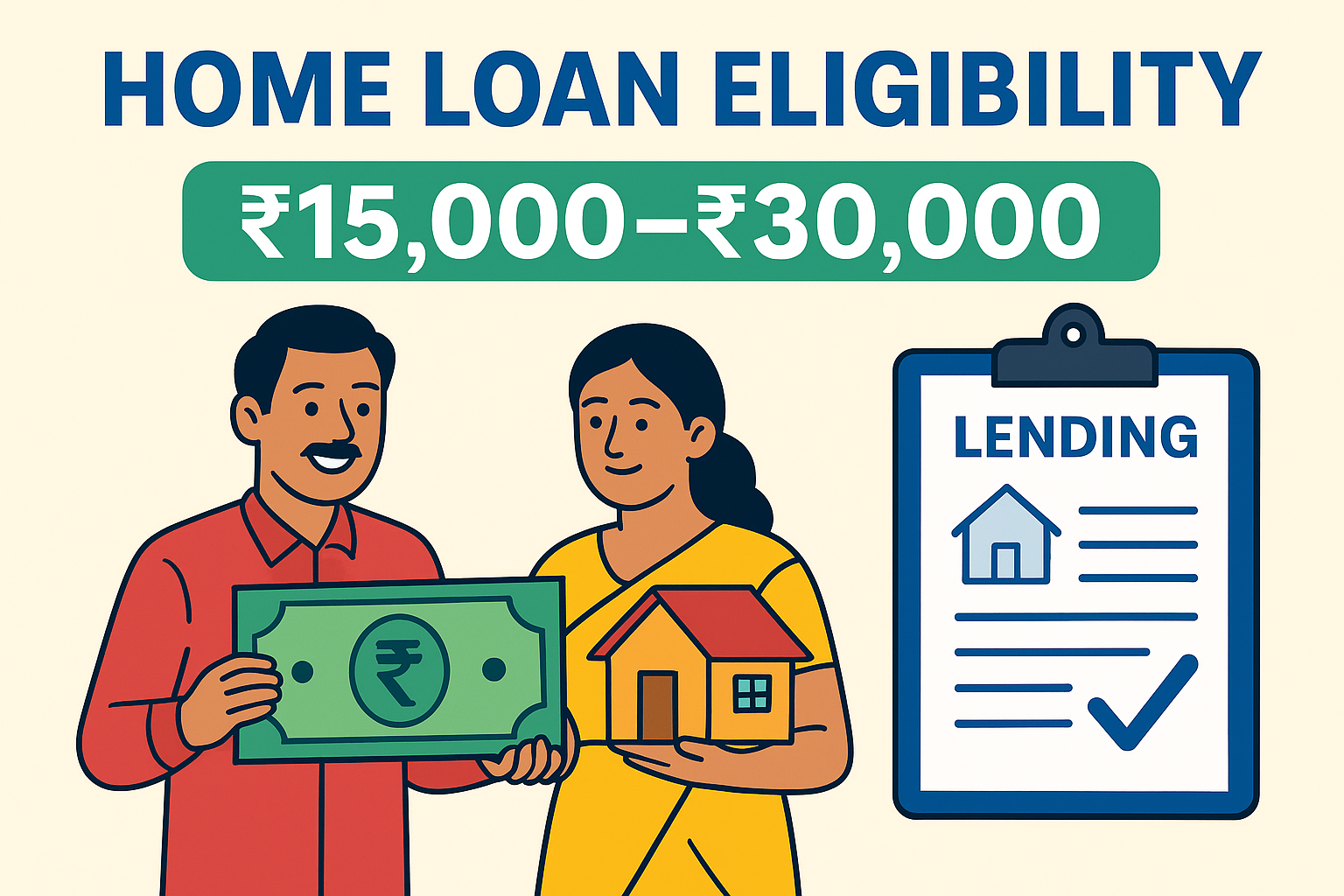

Owning a home is one of the biggest milestones in life. For many salaried individuals, it feels like a distant dream, especially when the monthly salary is modest. If you earn around ₹35,000 per month, you might wonder if you can qualify for a home loan and which banks will approve your application.

The good news is that you can get a home loan even with this salary if you plan wisely and understand how banks evaluate your eligibility. This guide will walk you through the process, top banks to consider, expected loan amounts, and 20 frequently asked questions to clear all your doubts.

- Home Loan Eligibility for ₹35,000 Salary

Banks and housing finance companies determine eligibility based on your income, credit score, age, job stability, and existing financial commitments.

General calculation:

Monthly salary: ₹35,000

Maximum EMI allowed: 40%–50% of salary = ₹14,000 – ₹17,500

Loan tenure: 15–20 years

Possible home loan amount: ₹20 – ₹30 lakh (approx.)

💡 Tip: Adding a co-applicant with a stable income can significantly increase your eligible loan amount.

- Top Banks for Home Loans in India

Here are some of the best banks and financial institutions for salaried individuals with moderate income:

Bank / Lender Interest Rate (p.a.) Special Feature

SBI Home Loan 8.00% – 8.75% Low processing fees & higher tenure

HDFC Home Loan 8.10% – 9.00% Flexible EMI options

Axis Bank Home Loan 8.20% – 9.05% Quick approval process

ICICI Bank Home Loan 8.15% – 9.05% Minimal documentation

LIC Housing Finance 8.30% – 9.50% Ideal for mid-income group

- Interest Rate Overview

Interest rates directly affect your EMI. For a ₹35,000 salary, look for home loans with interest rates between 8% and 9% p.a. Lower rates help reduce the total repayment burden.

- Documents Required

You need to keep these documents ready while applying for a home loan:

KYC Documents: Aadhaar card, PAN card, voter ID

Income Proof: Last 3–6 months salary slips

Bank Statements: Last 6 months

Employment Proof: Offer letter, Form 16, or HR letter

Property Papers: Sale agreement, builder documents, etc.

Photographs: Passport-size photos

- Tips to Increase Home Loan Eligibility

If your salary is ₹35,000, follow these tips to improve your chances:

- Maintain a credit score above 750.

- Clear existing loans or credit card dues.

- Opt for a longer tenure to reduce EMI burden.

- Add a co-applicant, like your spouse or parent.

- Keep a stable job history of at least 2–3 years.

- Make a higher down payment (20% or more).

- Down Payment Planning

Banks usually finance 75%–90% of the property’s value. You need to pay the remaining amount as a down payment.

For example:

Property value = ₹30 lakh

Bank loan = ₹24 lakh (80%)

Your down payment = ₹6 lakh

Start saving early to meet this requirement comfortably.

- Step-by-Step Process to Get a Home Loan

- Check Eligibility: Use an EMI calculator.

- Compare Banks: Look at interest rates and processing fees.

- Gather Documents: Prepare KYC, income, and property papers.

- Apply for Loan: Submit application online or offline.

- Verification: Bank will verify your documents and property.

- Approval: Once approved, sign the agreement.

- Disbursement: Loan amount is released to the builder or seller.

- Common Mistakes to Avoid

Ignoring credit score improvement.

Applying with multiple banks simultaneously.

Not reading the fine print on charges.

Selecting a short tenure that increases EMI burden.

Underestimating hidden costs like registration, stamp duty, and processing fees.

- Estimated EMI for ₹25 Lakh Loan

Loan Tenure Interest Rate (8.5% p.a.) Monthly EMI

10 years ₹30,997 High EMI burden

15 years ₹24,542 Balanced option

20 years ₹21,678 Lower EMI option

- Conclusion

A ₹35,000 salary is sufficient to qualify for a home loan if you plan carefully. With banks like SBI, HDFC, Axis Bank, ICICI Bank, and LIC Housing Finance, you can avail a loan of up to ₹25–30 lakh. Always maintain a good credit score, plan your down payment, and opt for a longer tenure to keep EMIs affordable.

With proper planning, your dream home can become a reality without putting too much strain on your monthly budget.

20 Frequently Asked Questions (FAQs)

Q1. Can I get a home loan with a ₹35,000 salary?

Yes, you can get a home loan if you have a stable job, a good credit score, and minimal liabilities.

Q2. What is the maximum home loan amount I can get with a ₹35,000 salary?

You may qualify for a loan between ₹20 – ₹30 lakh depending on the bank and tenure.

Q3. Which bank is best for a home loan with a moderate salary?

SBI, HDFC, Axis Bank, ICICI Bank, and LIC Housing Finance are great options.

Q4. How much EMI should I expect on a ₹25 lakh loan?

Approximately ₹21,000 – ₹25,000, depending on the tenure and interest rate.

Q5. What is the minimum credit score required?

A credit score of 750 or above is ideal for approval.

Q6. Can I get a home loan without a co-applicant?

Yes, but adding a co-applicant can increase your eligibility and loan amount.

Q7. How long should my job experience be to apply for a home loan?

Most banks prefer at least 2 years of continuous employment.

Q8. Can I include variable components like incentives in my salary?

Yes, some banks consider incentives or bonuses, but primarily focus on fixed salary.

Q9. What percentage of property value will banks finance?

Banks usually finance 75%–90% of the property cost.

Q10. Are there hidden charges in home loans?

Yes, processing fees, legal charges, and insurance costs may apply.

Q11. Can I prepay my home loan early?

Yes, most banks allow prepayment, but check if there are any penalties.

Q12. What documents are mandatory for salaried individuals?

Salary slips, bank statements, KYC documents, and Form 16 are essential.

Q13. How can I improve my home loan eligibility?

Clear debts, maintain a good credit score, and increase tenure.

Q14. Is it possible to get a home loan if my salary is credited in cash?

No, most banks require salary to be credited to a bank account.

Q15. Can I take a home loan for a plot purchase?

Yes, many banks offer loans for plot purchases under specific schemes.

Q16. What is the typical processing time for a home loan?

It usually takes 7–15 working days, depending on the bank.

Q17. Can I transfer my existing home loan to another bank?

Yes, through a home loan balance transfer, often to get lower interest rates.

Q18. Will a longer tenure increase my total interest?

Yes, longer tenures reduce EMI but increase total interest paid.

Q19. How much down payment should I plan for?

At least 10–20% of the property’s value.

Q20. Can I apply for a home loan online?

Yes, most banks now offer online application and document upload facilities.